M-Pesa’s Journey

Initially M-Pesa was a philanthropic journey. It was intended to make the MFI (micro-finance institutions) chores efficient (focus was initially on making the payment transfer digitalized). M-Pesa was co-funded by DFID and Vodafone. The business idea did not get the desired level of response at Vodafone as Vodafone’s primary focus was still on Europe and USA. Before, M-Pesa – mobile money’s profitability experiences were not very rosy. Smart Money’s (Philippines) and Celpay’s (Zambia) results were not really convincing. By 2003, margins (on SMS texting and voice calls) for Vodafone were around 38%. So, on benchmarking basis, M-Pesa did not have a stance. The current business model is inspired by the success of pilot survey.

M-Pesa initially stood out for a virtual money transmission model. It is neither a bank, nor any financial institution. In Kenya, it did not even get license from the central bank. Initially, there was no borrower-lender relationship approved under M-Pesa’s business model; no interest paid on deposits or loans. Initially there were caps on maximum account balance or maximum transaction size in order to reduce the risks of money laundering. Over time, Kenyan regulations became very conducive towards ensuring an enabling regulatory framework for MFS providers. Now, regulators have even allowed M-PESA (an MNO-led MFS model) to introduce formal banking (M-Kesho), micro-finance (musoni) and insurance products.

The unprecedented success of M-Pesa can be contributed to first-mover advantage. Safaricom – the platform and network provider had more than 80% market share in Kenya. 12% of Safaricom’s revenue comes from M-Pesa; M-Pesa broke even in 14 months. The gap between (% of population having a mobile phone and % of population having a bank account) is also too high in Kenya. It allows both the agents and Head office/ aggregators make ample commission.

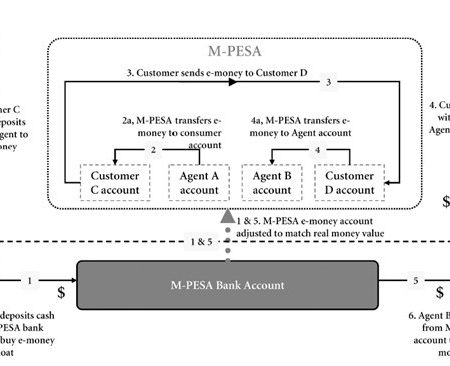

M-Pesa’s eco-system is multi-layered. At layer one, Safaricom works as the network & platform provider. Head-office, aggregator and super agent are the key ingredients of the next layer of the eco-system. Agent buys e-floats from Safaricom and enjoys 30% – 20% of the commission. Agents are geographically scattered; they communicate with the head office and aggregator. Head office and aggregator enjoys 70%-80% of the commission. Currently three MFS business models are working under M-Pesa’s eco-system simultaneously. Under the head office model commission distribution is head-office driven and head office owns agents. Under the aggregator model, commission distribution is Safaricom driven and the aggregator does not own agents. Under the super agent model, bank – branch manages cash and e‐float balances of a group of non‐bank M‐PESA agents.

Liquidity risks, network shutdown, agent specific risks are the basic risks to which M-Pesa are exposed to. Agents often run out of e-floats; since Keyna is highly geographically scattered it is costlier and time-consuming for agents to fill-up e-floats. Network shutdown (a problem linked up with Safaricom) needs huge investment to get sorted. Thefts, recovery of initial start-up cost are some key agent specific risks. Even though, through a trust-authority framework, a current account is maintained, but the deposit insurance coverage is extremely limited.

Leave a Reply